Do New Homeowners Need Mortgage Life Insurance?

Getting the keys to your moving in home is a thrilling moment. However, what is often initiated is a less than exciting flood of mail about Mortgage Life Insurance. You’ve just made the biggest purchase of your life and all of a sudden, everyone in the business wants to sell you a new policy. But what is it, really? And is any sense in it, financially, for you and your family?

This should be a definitive guide to find out and understand this often-misunderstood product. We’ll look at just what it does cover, how it compares to what else is out there and, why for most homeowners there is a much better way to protect your loved ones and your new home.

What Exactly is Mortgage Life Insurance?

Mortgage Life Insurance, commonly known as mortgage protection insurance (MPI) is a special kind of insurance policy. Its only purpose is to be used to pay off the balance of your mortgage if you die.

Sounds busy-body good on the face of it really, doesn’t it?

The concept is simple. You purchase a policy, you pay a monthly fee and if you die while the policy is in force, the insurance company will pay the outstanding mortgage debt directly to your lender.

Consequently, your family gets a mortgage relief. They get to keep the house without having to worry about foreclosure. However the details of how this works are of critical importance.

How Does the Payout Work?

This is the most important differentiation. Unlike traditional life insurance, with a Mortgage Life Insurance policy, the death benefit in it does not go to your family.

It is paid directly to the bank/mortgage lender.

Your loved ones never end up seeing the cash. While the mortgage is paid off, they have no flexibility in getting money to take care of other immediate needs. This lack of control is a major disadvantage which we will discuss in detail at a later point.

The Flood of Mail: Why Are You Being Targeted?

Shortly after closing on a home, most new homeowners are flooded with official looking letters. These letters tend to mention your lender’s name and the amount they said your loan owed, which will lead them to believe this is a sense of urgency.

So, how do they get hold of your information?

It’s surprisingly simple. When you purchase a home, your deed and mortgage papers would become public record. Insurance companies and marketing agencies legally obtain this data. They know your name, address, lender and original loan amount.

They use this information make extremely targeted and sometimes deceptive marketing campaigns designed to create a sense of urgency around Mortgage Life Insurance. Be suspicious of any mail implying that the policy is mandatory from your lender, in fact, it almost never is.

The Big Debate: Mortgage Insurance vs Term Life

Now we get to the question of central concern to homeowners. When you compare between mortgage insurance vs term life insurance, one of them always offers more value, flexibility, and protection for your family.

While Mortgage Life Insurance is for one specific debt, term life insurance offers a safety net for all the financial needs of your family.

So let’s try to deconstruct the basic differences. To get the picture we have made a small card with a simple comparative.

Comparison: Mortgage Life vs. Term Life Insurance

| Feature | Mortgage Life Insurance (MPI) | Term Life Insurance |

|---|---|---|

| 💎 Beneficiary | The mortgage lender (your bank). | Your chosen loved ones (spouse, children, etc.). |

| 📉 Benefit Amount | Decreases as you pay down your mortgage. | Remains level for the entire term (e.g., $500,000). |

| 💰 Premium Cost | Stays the same, even as the benefit shrinks. | Stays level for the entire term. |

| ✨ Flexibility of Payout | None. The money can only pay off the mortgage. | Total. Family can use the cash for anything they need. |

| 🔄 Portability | Often not portable. If you refinance, you may lose it. | Completely portable. It’s tied to you, not your loan. |

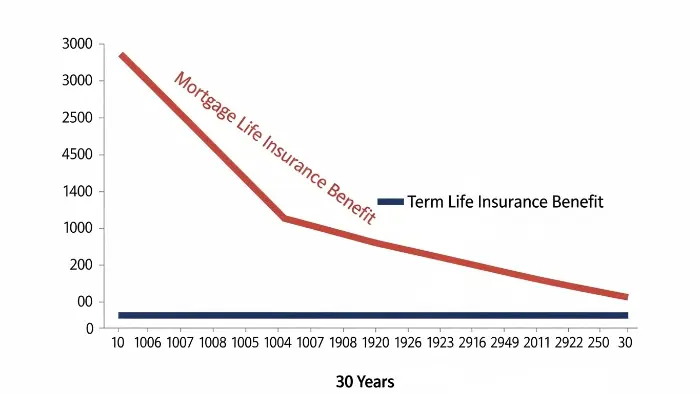

Drawback #1: The Decreasing Payout of Mortgage Life Insurance

The biggest weakness of the standard Mortgage Life Insurance policy is the diminishing benefit. In fact many of these policies are a form of decreasing term life insurance.

Here the way it works is your amount of coverage directly relates to your mortgage amount.

As you make your monthly mortgage payments, your loan amounts decline. Consequently, the death benefit of your insurance policy is decreased as well.

However, your monthly premium will almost always remain the same.

You are paying the same price for a benefit which is constantly shrinking. After the course of 30 years or you’ll be paying the same premium on the tiny fraction of the original coverage. This is a horrible return on your investment.

Drawback #2: The Beneficiary Isn’t Your Family

We’ve touched on all this but is worth repeating. The creditor of the Mortgage Life Insurance is the bank. This is a critical point that many people fail to see.

Think of the financial mayhem that ensues following a death.

Your family may require money for other expenses such as funeral, medical bills, or just normal living expenses. They may need some time to grieve without immediately having to go back to work.

If the insurance payout goes straight to the lender, you are left with a family who has paid off their house, but may have no cash to deal with these immediate crises. A traditional term life policy allows them the freedom to make decisions on how the money best can be used.

Drawback #3: The Higher Cost (The MPI Cost Trap)

For the small and shrinking amount of benefit that the Mortgage Life Insurance offers, it is in many cases surprisingly expensive. The MPI cost is quite high compared to a similar term life insurance policy.

Why is this?

One main reason is through underwriting process. MPI usually sells with “simplified” or “guaranteed” underwriting which means there is no medical exam. In order to compensate for the risk of providing insurance against an unforeseen accident such as death or injury to someone who is not healthy, it is the insurance company’s policy to charge everyone high insurance rates.

If you are relatively healthy, then you are essentially subsidizing the cost to higher-risk people. This means that you are paying too much for less coverage. It’s much better to have a simple medical exam in case of a term life policy and get a much lower premium. The impact of your health on health insurance premiums is similar, better health means better rates.

As financial guru Dave Ramsey says: “Mortgage life insurance is a rip-off. It’s an easing benefit that you’re paying for a level premium on. Don’t buy it.”

The Superior Alternative: Term Life Insurance for Homeowners

For for the great majority of people, the best form of life insurance for homeowners is a standard level term life insurance policy. It’s more affordable, more flexible and deliver far greater value.

term life insurance is unquestionably beautifully simple.

You select a coverage amount (i.e., life insurance payout, e.g. $500,000) and a term length (e.g., 10, 20, or 30 years). Your premium will stay at the same level as will your death benefit over the course of the term.

If you die when you have been on the policy for some time, your beneficiary, your family, receive the full, tax-free cash benefit.

The Power of Flexibility

This is the best merit of term life insurance. When your family receive the death benefit, they are in total control.

They can opt to pay off mortgage early. This is definitely a great and popular choice.

However, they also could make the decisions to:

- Use a part of it for immediate expenses of living.

- Invest the money so it can generate never-ending income.

- Pay off other debts; such as car loans or student loans.

- Provide college education right for the children.

- Save money for emergency occurs in future.

This is flexibility that is priceless in a difficult time. It empowers you to find the best decisions for your unique situation; not being limited to one choice to make. The process of finding the right amount of life insurance coverage is important in order to ensure that all of these needs are met.

Getting More Coverage for Your Money

Being medically underwritten, term life insurance can be used to obtain a large amount of insurance for very little cost to the insured if the individual is healthy.

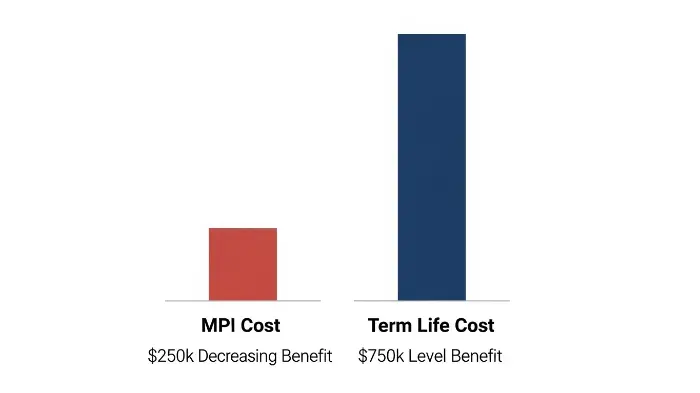

For instance, a healthy 35-year-old could pay the same monthly premium to buy $250,000 of Mortgage Life Insurance as he would for a $750,000 30-year term life policy.

For the same cost you receive triple coverage.

Furthermore, that $750,000 benefit never falls. It’s an amazing tool to have in terms of saving your family’s your whole financial future and not just the house. This makes the term insurance vs whole life insurance debate even more relevant with term insurance winning hands down in terms of mortgage protection.

Let’s Talk Numbers: A Real-World Cost Comparison of Mortgage Life Insurance

Coming to make this real with a hypothetical scenario.

Meet Sarah, a 35 year old female, non-smoker, who is in excellent health. She just purchased a home with a 30 year, $400,000, mortgage.

Option 1: Mortgage Based Life Insurance

- Coverage: $400,000 Decrease of Benefit.

- Term: 30 years.

- Estimated Monthly Premium: $65 – $85.

- Benefit in Year 29: It will be approximately $40,000 (but her premium is now still $65+).

- Beneficiary: The Bank.

Option 2: 30-Year Level Term Life Insurance

- Coverage: $1,000,000, level benefit.

- Term: 30 years.

- Estimated Monthly Premium: $50 – $70.

- Benefit in Year 29: Still $1,000,000.

- Beneficiary: Sarah’s Husband & Children.

The choice is stark.

For a lower monthly cost, Sarah is able to supply her family with two and a half times the initial coverage, and the coverage never decreases. This is why financial experts almost universally recommend term life over any type of Mortgage Life Insurance plan.

Checklist: Is Mortgage Protection Insurance Right For You?

Answer these questions honestly. If you answer “Yes” to most of these, a standard term life policy is likely a much better fit.

👨👩👧👦 Do you want your family (not the bank) to receive the insurance payout?

✨ Do you want your family to have the flexibility to use the money as they see fit?

⚕️ Are you in good health and willing to take a medical exam for a lower rate?

💰 Do you want your coverage amount to stay the same for the entire policy term?

🔄 Do you want a policy that stays with you even if you sell your home or refinance?

When Could Mortgage Life Insurance Potentially Make Sense?

When is it ever a time to consider Mortgage Life Insurance? There is one very narrow situation in which it is a last-resort:

This is for people who are suffering from serious, pre-existing health conditions which prevent them from being insured for a traditional term life policy.

Because MPI oftentimes has guaranteed or simplified acceptance, it can be a way for someone in very poor health to get at least some coverage for their mortgage debt. However, even if that is the case, you should first explore all other avenues.

Work with an Independent Insurance Broker. They can shop your case with various carriers including those that specialize in high-risk applicants. You may be surprised at the things available. Options such as simplified issue or guaranteed issue term life insurance plans may still be a better deal.

A Closer Look at the Fine Print of Mortgage Life Insurance

Beyond the big picture issues, there can be other disadvantages hidden in the fine print of a Mortgage life insurance policy.

One of the biggest problems is portability. Your policy is attached to a particular mortgage.

So, what happens if you think of refi your loan for a better interest rate? In many instances, your MPI policy will be terminated. You would then have to re-qualify at a higher age for another policy which invariably implies higher premiums.

A term life policy on the other hand is totally portable. It is yours, no matter what your mortgage, your job is, or where you live. You can even refinance or even sell your home and move and your coverage follows you.

The Underwriting Process Explained

Underwriting is the process employed by an insurer to check the risk factor and determine the amount that you have to pay.

For the purpose of Mortgage Life Insurance, such as stated before, this is usually a simplified questionnaire without any medical exam. This convenience has come at a high price.

For term life insurance, the process is more in-depth. It typically involves:

- A detailed application.

- A review of your health care records.

- Medical exam (height, weight, blood pressure, blood/urine sample) – free of charge, in-home.

While it sounds like a bunch of extra hassle, the process is meant to ensure that the insurance company can correctly pain an accurate picture of your health. For healthy applicants, this places them in one of the lowest cost MPI (compared with the one-size-fits-all pricing of MPI). For those wanting coverage, it’s always wise to compare coverage with the best life insurancesto ensure that you end up with the best rates.

Expert Opinions on Mortgage Protection Insurance

The consensus views of personal finance experts are overwhelmingly clear and in line with the above analysis.

The famous financial advisor Suze Orman called these policies “one of the biggest rip-offs in the insurance industry” more than once. She promotes term life insurance because it provides control to your family.

Similarly, an article from Investopedia says that “for most people, a term life policy is the better option” because it “provides a death benefit to the beneficiaries they name, who can then use the money for any purpose.”

The experts say – protect your family, not Does cause your lender. This is done much better with a robust term life policy, than with any of the Mortgage Life Insurance products.

Beyond the Mortgage: Building a Complete Financial Safety Net

Your mortgage is probably your biggest debt but it’s not your only financial responsibility. A proper financial safety net should be a story of your family’s whole picture.

This is another zone where term life insurance springs.

When it comes to calculating your coverage needs, you need to be thinking out of the box when it comes to your mortgage. A good rule of thumb is to get the death benefit equal to 10-12 times your annual income. This amount can help to support your family:

- Pay off the mortgage.

- Replace your lost income for a decade or longer.

- Finance your children’s future education.

- Pay every debt that you have (cars, credit cards, student loans) off.

- Cover final expenses; funeral costs.

A Mortgage Life Insurance policy can’t do any of that. It’s a one trick pony, in a world of three and four talent required work horses. It’s also important to check your health coverage, as many people find that their employer’s group health insurance just isn’t fully sufficient to them and a look at private health insurance plans is necessary.

Don’t Forget Disability Insurance

It’s also very important to consider another risk: disability. According to Social Security Administration, a 20-year old has a 1/4 chance of becoming disabled before reaching full retirement age. You are much more likely to be injured and not be able to work than to die during your working years.

Disability insurance is where they will protect your income in case you can’t work from illness or injury.

This is an important piece in the jigsaw. If you’re disabled, the mortgage payments don’t stop. A disability policy gives you access to the monthly income you need to continue paying your bills, including your mortgage, while you get better. Protect your family’s lifestyle at a time when you are still living. Like other insurance products, a good policy may even reward you with a no-claim bonus in the long run.

How to Find the Right Life Insurance for You

Feeling Belize there to go completely with term life? The process of acquiring it is simple enough.

Step 1: Calculate Your Needs. Don’t just guess. Use an online calculator or seek the help of a financial advisor to make the right choice about the amount of cover you need for your family. Think about the mortgage, income replacement and future goals. A resource like this post from NerdWallet to the life insurance calculator can be a great beginning.

Step 2: Compare Quotes. Don’t buy from the first company you see. Rates may differ significantly from one insurer to another. Use an independent on-line broker or work with an agent representing more than one company to get the best value.

Step 3: Apply and Complete the Exam. Be honest on your application. The short medical examination is simple and conducted at your own pleasure. This is the secret to setting the lowest possible rate. It’s much simpler than having to make a car insurance claim after an accident.

This process ensures that you get a policy that fits your needs and budgets and that they will offer maximum protection for your loved ones. As a last resort for those concerned about high premiums because of pre-existing conditions, a Dave Ramsey-endorsed provider such as Zander Insurance will go shopping for policies for high risk.

Conclusion: Your House, Your Choice, Your Family’s Future

Buying a home is more about generating a future for your family. The financial tools that you choose should help in that goal. While Mortgage Life Insurance is sold as a way to protect that dream, it has the tendency to be falling short of protecting the dream of your family and more the dream of the bank. The diminishing benefit and high cost, as well as its inflexibility make it an inferior choice in most, if not all, cases. A level term life insurance policy is, therefore, a much better, more flexible and cost-effective solution.

It empowers your loved ones with the financial freedom to more than just keep their home that are ‘temporarily’ offered to them by ‘temporary’t loans that work out well until during a snowstorm enjoying the rain, but when the snow storm of life strikes, they have no way of protecting themselves from the torrential coming snow but protecting themselves from the torrent of the snow, by the grace of the storms of the State. Ultimately, one of the best ways you can protect your new home is to first protect the people who live in it and having a comprehensive term life policy is definitely a better tool for the job than Mortgage Life Insurance.

Frequently Asked Questions (FAQ)

No, they have completely different. Mortgage Life Insurance (MPI) is a policy that is offered on an optional basis that will pay off your mortgage if you die. Private Mortgage Insurance (PMI) is regularly necessary by lenders in case your down payment is smaller than 20 percent. PMI protects the lender if you default on your loan & is no benefit to you/ your family.

While it’s easier to get than traditional life insurance, however, you can be turned down. Most simplified policies regarding issues request a few health questions. If you experience a recent history of considerable diseases such as cancer or heart disease, you may not be accepted.

The policy terminates. It is attached to that particular mortgage loan. You do not get any reimbursement of the premiums that you paid. This is another reason why a portable term life insurance policy is a better long term asset.

No, in nearly all cases, personal life insurance policies premiums, including Mortgage Life Insurance and term life insurance are not tax-deductible. They are treated as a personal expense.

The exam is also a rapid and convenient process. A licensed paramedic arrives to your home or your office at a time of your choice. The process usually lasts around 20-30 min and consists of measuring the height and weight, measuring your blood pressure as well as obtaining a small sample of your blood and urine.