Benefits of Pay As You Drive Car Insurance for Low Usage Drivers

Are you tired of high car insurance premiums? You may not drive your vehicle much at all. Perhaps work from home is on the cards now. Or maybe you’d rather use public transportation to go about your daily commutes.

And if this sounds like you, then traditional car insurance can seem unfair. You are paying just as much as one who drives constantly. But what if there was another way that was better? This is where Pay As You Drive Car Insurance comes in. It is a revolutionary approach to insurance.

This type of policy correlates your costs directly to your usage of the car. So, you are paying for what you actually use. It is a fair and flexible alternative. However, in this guide, we will teach you everything you need to know.

But we will discuss how it works and what are most of the people who benefit by it. Consequently, you can determine whether it is the correct decision for you. Let’s plunge in and discover how you can begin saving.

What Exactly is Pay As You Drive Car Insurance:

You may have heard the term but asked yourself what does it mean? Let’s put it down in terms of simplicity. This model of insurance is a massive change from the old way.

The Core Concept of Usage-Based Insurance

Pay As You Drive Car Insurance is a form of usage-based insurance. The main idea is very simple. Your insurance premium is determined by how much you are driving. If you drive less you should pay less. It’s a good system of equality for many people.

Traditional insurance has broad factors. These include your age, model of the car and your driving history. It is assuming the average mileage. This is not true for many people. So for example, a low-mileage driver pays for miles that they never drive. This new model corrects for that problem.

How Does It Work: The Technology Behind Telematics Car Insurance

So, how does your insurer know the number of miles that you drive? The answer is technology. In particular, it employs a field known as telematics. Telematics car insurance is the backbone of this whole system. It is a combination of telecommunications and informatics.

It is installed in your car to have a tiny device. This device is used to collect and send driving data. The insurer then utilizes this data. They work out a premium based on what you really use. It is a very accurate and individualistic method. This is a far cry from needing old, generalized premium calculations.

The Telematics Device (The “Black Box”)

The most common method is “black box.” This isn’t as scary as it sounds however. It’s a small device and is roughly the size of a deck of cards. A professional on installation of the system on your car is a breeze. Usually, it’s put unobtrusively and out of manifestation.

Once the device is installed it gets to work. It monitors different bits of information regarding your driving. This includes, of course, your mileage. However, it can also be used to track other factors. We shall discuss those in more detail subsequently. This data is a complete picture of said habits of your driving.

The Smartphone App Alternative

Some insurance companies now have a less complicated alternative. They have smartphone apps that are able to do the same job. You just download the app. Then, you assign permissions to it which are necessary. The app is based on the GPS and sensors of your phone. Your trips are automatically tracked by it.

This is an excellent option to many. It does not require any hardware installation. This makes it so convenient to start. However, it does mean that the app needs to be on when you drive. It also consumes the battery and data of your phone.

The Major Benefits of Pay As You Drive Insurance

Now, let’s get to the best part. What are the actual benefits to you – the driver? The advantages are great, especially in some lifestyles. This is why it’s getting so much popularity.

Significant Cost Savings: The Primary Appeal of Pay Per Mile Insurance

The number one benefit is saving money. For the low-mileage drivers, the savings can be enormous. With pay per mile insurance, your bill consists of two parts. There’s a low base rate. Then, there’s a little charge for every mile that you drive.

Imagine a situation in which you only drive 5000 miles in a year. Your premium will show that your low number. Someone that drives 15,000 miles is going to pay more. This direct connection of use to cost is the key. For many, this could save them money equal to half of their insurance bill. But it seems a lot more fair, doesn’t it: As you can see, the possibilities of car insurance savings are large.

“The future of insurance is personal. Technology is enabling us to make products that are truly tailored to the individual’s needs and behaviors.”

– Industry Analyst

Thinking about having insurance is not only for cars. It pays to think about your future in more ways as well. That’s why a number of millennials are taking a new look at life insurance options.

Are You a Good Fit for Pay-As-You-Drive?

You Work From Home

Your daily commute is a walk to the next room.

You Own a Second Car

It’s used only for occasional weekend trips.

You’re a Student

Your car stays parked on campus most of the time.

You Use Public Transit

The car is just for groceries and errands.

Rewarding Safe Driving Habits for Lower Premiums

This type of insurance has little to do with how much you drive. It’s also about how you drive. There are many policies where safe driving rewards are available. The telematics device can monitor your driving behaviour.

Do you avoid harsh braking? Do you accelerate smoothly? Staying within the speed limit is also done by you. These are indications of a safe driver. Insurers love safe drivers. Therefore, they reward for this behavior with even more decreed premiums.

This allows you another level of control over your costs. You are now in the driver’s seat when it comes to your insurance bill. It’s also an incentive to become a safer driver which also benefits everyone. This is a sure way to achieve a low mileage discount.

Transparency and Control Over Your Insurance Premiums

Have you ever gotten lost with your insurance bill? You get a renewal notice and the price has increased. But you don’t know why. Pay As You Drive Car Insurance changes that. Most providers have either a dashboard or an app available online.

You will find all your trip data here. You can see how much you have bought for the month patiently. Your scores for driving can be viewed by you. It’s all laid out clearly. This is like a power of transparency. You know what exactly you are paying for. Furthermore, if your premium changes, you understand the reason for such a change. Understanding your policy is very important as is knowing the details of riders in life insurance plans.

Perfect for Specific Lifestyles of Occasional Drivers

This insurance is a perfect fit for certain people. It’s ideal for insurance for occasional drivers. If you fit one of these groups you better pay close attention.

- Remote Workers: There has been a huge increase in the amount of people working from home. The daily commute is a thing of the past to many. Their cars now sit idly around for most of the week.

- Retirees: Many retirees do not drive nearly as much as they used to. Trips are usually local and not very frequent.

- Students: A student who lives on campus might only use his or her car on holidays. Doing a standard premium makes no sense.

- Urban Dwellers: If you live in a city that has really nice public transport systems, your car might be a weekend only luxury.

For all these groups, the savings may be dramatic. It finally makes insurance seem fair and logical.

Is Usage-Based Insurance the Right Choice for You?

While the benefits are not in dispute, it’s not right for everyone. One thing you need to do is to evaluate your own driving habits. Let’s have a look about who is looking to gain the most. And, just as critically, who mightn’t.

Who Benefits the Most from this Model:

We’ve touched on this already. But let’s get more specific. You are an ideal candidate if you relate to the outlines of these profiles. The less you are out on the road, the more you have to save.

The Urban Dweller with Public Transport Access

Living in a big city has its advantages. You have trains, buses and subways. Your car is for to go for specific trips. Perhaps you use it for a big running grocery run. Or for visiting family out of the city. On a daily basis it remains in its park position. You are paying for insurance amid a car that is seldom used. This is a policy that may be a game-changer for your budget.

The Stay-at-Home Parent or Remote Worker

Moving through your body Your daily “commute” is from the bedroom to the living room. Or maybe you’re a parent whose driving amounts to driving the kids to and from school and going out to the local store. You annual mileage is well below the national average. With the traditional policy, you are punished. With a Pay As You Drive Car Insurance policy, you are rewarded for your lifestyle.

The Weekend Adventurer with a Second Car

A large number of households own more than one car. One is the daily driver. The other is for fun. It could be a classic car or convertible. It only comes out on sunny weekends, however. Insuring this second car can cost a lot. With a based on use policy, you only have to pay for those weekend miles.

Students and Young Drivers

Young drivers generally experience the greatest premiums. They are viewed by insurance companies as high-risk. But a student who leaves his or her car at home is no risk. Or one who never drives much while at college. This is a policy that helps them to prove that they are low-mileage drivers. It can result in a much more affordable coverage. It is good for young people to have some understanding of the various types of insurance, just as it is to know what is term vs whole life insurance.

Who Might Not Benefit?

On the other hand, this is not a magic solution for all drivers. Some people probably ought to stick to a traditional plan.

If you are a high-mileage driver, then this is not for you. Sales people, delivery drivers or long distance commuters will not save money. In fact, you may end up spending more. The per-mile charge would add up very quickly. Similarly, if you have an unpredictable driving schedule then you might want the reassurance of a flat rate. Also, some people are not comfortable with the data-tracking aspect, which is a valid concern which we will proceed to address next. It is important to know your family’s needs, much like how you need to calculate your life insurance coverage.

Understanding the Data: What Does Telematics Track?

Privacy is a very big issue in our digital world. So, it’s only natural to ask what data is being collected. It’s important to be informed. Let’s lift the veil on telematics data.

“What gets measured, gets managed. By tracking driving habits, telematics not only helps insurers but also encourages safer roads for everyone.”

-Forbes Advisor

It’s More Than Just Miles: Key Data Points

While mileage is the major factor, of course, it’s not the only one. The device or app can track a number of things to gauge your level of risk.

- Speed: Are you always going over the speed limit? This indicates higher risk.

- Acceleration and Braking: Acceleration with excessive force and stopping without a wide and gradual distance may reveal impatient driving. Smooth driving is safer.

- Time of Day: Nighttime driving statistically is riskier. Some policies factor this in. Driving at peak rush hour can be a factor as well.

- Cornering: Taking corners too fast is another indication for risky behavior.

- Location (GPS): The device knows where it is that you are. This can help log your miles, so that you can log them accurately. It can also be a lifesaver. Many telematics services incorporate emergency assistance and stolen vehicle tracking services.

Addressing Privacy Concerns with Telematics Car Insurance

Insurance companies know that privacy is a huge issue. They have some strict policies in place. The data collected is only used for calculation of your premium and for the provision of related services. And, they are not selling your location data to marketers.

Think of it being like a smart thermostat. It learns your habits to save you on the cost of heating. A telematics device feeds you back in terms of your driving habits in order to save you money on insurance. Reputable insurers let you know what they do about their data.

You always must read through terms and conditions carefully before signing up. For more detailed information on insurance plans, you may be able to learn more from articles on the best family health insurance plans.

Your Road to Savings

Low Monthly Base Rate

Per-Mile Rate

Total Monthly Premium

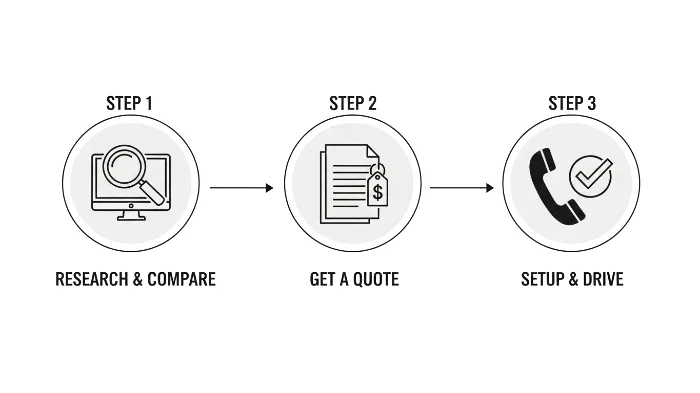

How to Switch to Pay As You Drive Car Insurance

Are you one to convince that might be for you? Making the switch is not as difficult as it may seem. Here is a basic guide to help get you at the beginning of the savings road.

Step-by-Step Guide to Making the Change

Switching your car insurance doesn’t believe it be a headache. Just do a few logical steps and you will find it. A little research now, can result in big research later.

Research and Compare Providers

First of all, not all insurance groups have this type of insurance. You have to find the ones that do. Major companies, such as Progressive (Snapshot) and Allstate (Drivewise), have programs. There are also specialized companies such as Metromile and Noblr. A great outside resource for comparison is NerdWallet’s analysis.

Have a look see their specific offers. Do they make use of a plug-in device or an app? What is their base rate, and per mile charge? Do they sell safe driving discounts? Read the reviews of other customers.

Getting a Quote for Your Car

Once on a shortlist, get quotes. This is usually easy to do on the Internet. You’ll be giving your personal information. You’ll also provide information on your car. You will have to determine your annual mileage. Be honest here. A bad (low) estimate will appear good in the beginning but will be corrected when tracking is implemented.

Compare the quotes that you receive. Look at the cost may be, of the whole potential cost. Don’t solely concentrate on the per mile rate. The base rate is also quite important. This process is similar to that of checking how are health insurance premiums affected by various factors.

Installation and Setup Process

After you select a provider, he or she will walk you through the set up. If it’s a plug-in device they will send it to you by mail. Usually, it will plug into the OBD-II port in your car. This port is standard on cars made after 1996. Usually it is found on the underside of the dashboard. It’s a very easy plug and play model.

If it’s an App based system, you just download it. You will be creating an account with following the instructions on the screen by hiring your. Then, you are ready to hit the road. Your saving journey has now started officially. If you ever have to use your insurance, knowing how to even begin filing a claim is your next important step.

The Future of Car Insurance: Is This the New Norm?

Technology is transforming each and every industry. Insurance is no exception. Pay As You Drive Car Insurance is not just a fad. It’s possible that it will be the way we insure the vehicles in the future.

“The road to the future is paved with data. Insurers who harness it to create fairer, more customer-centric products will lead the way.”

– PWC Global Insurance Report

The Rise of Usage-Based Insurance Policies

The number of usage-based insurance markets is growing rapidly. An increasing number of drivers are coming around to the benefits. They are insisting on fairer and more personalised products. Insurers are responding to this demand. They are spending a great deal of money on telematics technology.

As cars are also becoming “smarter” with connectivity built right in, this will become even easier. New cars may soon come with the technology already built in. This would make signing up for a usage based policy a breeze. And finding the right policy is just as it is in finding the best life insurance companies.

Impact on the Insurance Industry

This shift is forcing the industry to get innovative. Traditional, one-size-fits-all policies are falling out of date. Insurers need to become more like tech companies now. Managed to take care of data, develop apps and think about the user experience.

This is a good news to consumers. It means more competition and better products. It also helps in promoting safer driving. When drivers are rewarded for being safe, then the roads are safer for all of us. This is a very powerful side effect. Similarly, understanding on the advantages of a no-claim bonus in health insurance also pays off for good behaviour. For more on different types of policies you might look at the key difference between group health and individual policies.

Final Thoughts on Pay As You Drive Car Insurance

Pay As You Drive Car Insurance is the new, fair way to insure your vehicle. For the millions of low mileage drivers, it is a great opportunity. You can finally put an end to overpaying for insurance. You can get the power to manage your premiums by your driving habits.

It offers a considerable cost saving. It rewards safe driving. And it provides unparalleled transparency. While it is not the ultimate fit for every single driver because there is simply no chance at improving everyone, its benefits are surely there for many.

If you work at home or take public transit or just don’t drive a lot, then you owe it to yourself to investigate this option. Get a few quotes. Compare the amount of potential savings. You may be very surprised how much you can save. Get control over your car insurance costs NOW.

Frequently Asked Questions (FAQs)

No, it’s not even available in every state and from every insurer yet. However, its availability is rapidly increasing due to the growing number of companies which are adopting the technology. You should check with providers of your specific area.

It’s possible. If you do not have consistent speeding or aggressive driving making this data, you will not see a savings. Some policies may even impose a rate higher than a normal one for extremely risky drivers.

Most policies have a cap on the number of miles driven each day. For instance, they may only require you to pay for the first 150 or 200 miles that you drive in one day. This way you don’t end up spending one road trip with a bill that is dreadfully out of control.

No. The device is made to plug into the car’s standard OBD-II port. It’s an easy to use and low power data reader. It does not interfere with the working of your car and is totally safe.

Your driving information belongs to the insurance company you had the policy with. When you terminate your policy, collecting takes a halt. The new insurer will have a new start with their own device or app. No old data transfers your old data.