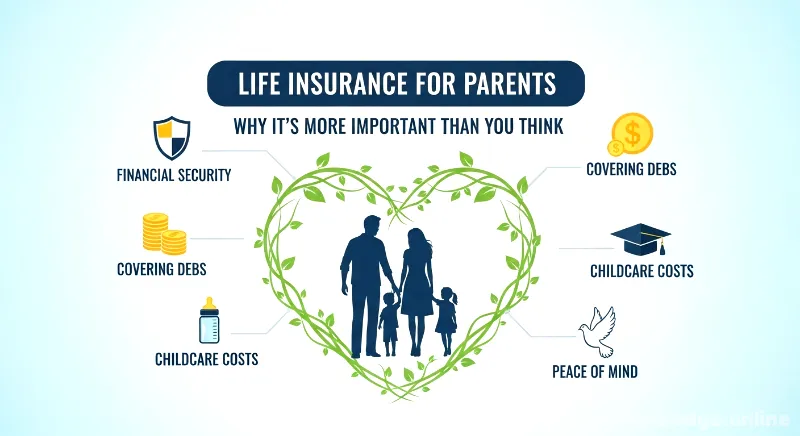

Life Insurance for Parents: Why It’s More Important Than You Think

Having the talk about money with our parents is sometimes tough. But having the conversation about Life Insurance for Parents is a conversation worth having. It’s such a topic that will elicit uncomfortable feelings. And we don’t want to think about a time when they’re not going to be with us.

Yet, please planning for that possibility is one of the most loving things that we can do. It helps give a shield for the future of our family. This plan allows making sure grief isn’t made worse by financial stress.

This guide will allow you to go through it all. We will cover the reason why it is so important. We’ll examine the various forms of policies. You will come to know how to choose the right one. Our formula is to explain this process in a simple and understandable way for you.

Why We Need to Talk About Life Insurance for Parents

The conversation can feel sort of awkward. But to avoid it can have serious consequences. A lack of planning can get a family into a difficult spot. They could have unexpected debts and final expenses. These costs can be added up very quickly.

Life Insurance for Parents provides one solution. It’s a financial safety net. It ensures that money is available in needful time. This is not about making money off of loss. It goes back to the survival of the people left behind.

It is about allowing your family an opportunity to grieve, without having to pay for their grief. For many this is a topic that is considered at an early point. In fact, life insurance on the millennials is something many millennials should keep in mind to secure a lower rate, and this applies to parents as well.

Understanding the Core Purpose of Parent Coverage

So, what does parent coverage really achieve? At its heart, it’s a promise. It is a promise of caring for your family even after you are no longer there to provide for them financially. The death benefit from a policy can be used for a lot of things. It is used for emergency expenses which provides immediate funds to where the money is needed.

This financial tool is remarkably versatile. It can pay for funeral costs. Outstanding medical bills can be saved by it. It can even be used to pay off a mortgage or other debts. For some families, this is replacing loss of income. The whole point is obvious: provide stability in a time of great instability. This is the spirit of the true family protection.

Covering Final Expenses and Debts

One of the most immediate expenditure uses for a life insurance payout is final expenses. You may find your educational plans at the cost to your surprise. The cost of the average funeral in the United States may range from $7,000 to $12,000. This doesn’t even include other end-of-life costs.

There may be outstanding medical bills. Or perhaps there are credit card debts. Without a plan, these costs fall on the members of the surviving family. Life Insurance for Parents can take this heavy burden off the shoulders. Through a policy, these final bills are paid. It entails the security of your family’s saving.

Providing Income Replacement for Dependents

What if one of your parents is still working? Or what if a surviving parent relies on their spouse’s income/pension? The loss of that income can be devastating. It can transform the life of a family overnight. This is where family protection comes in vitally.

A life insurance policy can help to replace that lost income. It provides the surviving spouse or dependents with breathing space. They can use the funds to cover their daily bills. It gives them time to adjust to their new reality. Before purchasing a policy, it is a good idea to determine your needs for life insurance to ensure that the amount is sufficient.

The art of living lies in knowing when to swallow up the pride and in knowing when to let it go. The art of financial planning is to ensure that your loved ones can forget about financial problems.

Different Types of Life Insurance for Parents

The Life Insurance Is Not All the Same. There are along a number of pipelines that are available. Each one of them is made for different needs and budgets in mind. The two most popular types are Term Life or Whole Life insurance. Understanding them is your first step.

This is a big decision to pick the right tried type. It depends on the age, health and financial goals of your parents. Do they require coverage for a particular length of time? Or do they need it for their entire life. Well, let’s break down the choice of the main ones.

Term Life Insurance: A Cost-Effective Choice

Term life insurance is very simple. It offers coverage for a specific period of time, or “term.” This could be 10, 20, or 30 years. If the insured dies during the period, the policy will pay out. If they outlive the term than the coverage ends.

The most important of these is affordability. Term policies are much less costly than permanent policies. Which makes them a great option for a lot of families. It’s great for paying for temporary debts such as a mortgage. It offers a huge amount of coverage at a low premium. Understanding important differences between term vs. whole life insurance can help in making an informed choice.

Whole Life Insurance: A Lifetime of Protection

Whole life insurance is a permanent insurance. As the name indicates, it offers a coverage to the insured’s entire life. As long as you pay the premiums the policy will pay out. This gives a great deal of certainty.

Whole life policies are more costly. However, they come with an added benefit, which is cash value. A fraction of your premium is set up in a savings account. This is a cash value which grows over time, tax-deferred. You will be able to borrow against it or even surrender the policy for the cash.

Term Life

- Coverage: For a fixed term (10-30 years)

- Cost: Lower premiums, very affordable

- Cash Value: No

- Complexity: Simple and easy to understand

Best for covering specific debts like a mortgage or providing for young children.

Whole Life

- Coverage: Permanent, for life

- Cost: Higher premiums, fixed for life

- Cash Value: Yes, it grows over time

- Complexity: More complex, a financial tool

Best for estate planning, leaving a legacy, and covering final expenses.

Exploring Senior Insurance Options

What if your parents are older, say, over 60? It can be more difficult to obtain more traditional life insurance. But it is not impossible. There are certain products suited to this age group. This category is often referred to as the senior insurance.

These policies take into account that the older applicants can suffer from some health-related problems. They are designed for people to be easier to qualify for. The quantities of coverage are typically less. The emphasis on income replacement is shifted to other needs. It’s about making sure the end of life costs are borne. This gives a tremendous amount of peace of mind.

Final Expense Insurance: Covering End-of-Life Costs

Final expense insurance is a very popular choice for senior insurance. It’s a small whole life policy. The amount of coverage is usually from $5,000 to $25,000. The goal is simple and direct. It’s aimed at covering funeral expenses, burial expenses and other final expenses.

One of its largest advantages is its accessibility. Many final expense policies do not provide a medical exam. Applicants also just need to answer some health questions. This makes it a great choice for those parents who may not qualify for other plans.

Guaranteed Issue Life Insurance

For the parents that have significant health problems there is another option. It’s called a guaranteed issue life insurance. As the name suggests, they can not be turned down. Acceptance is guaranteed although typically for the age of 50 to 80.

There is a catch, however. These policies have a “graded death benefit.” This means if during the first two or three years the insured dies from natural causes, the policy only returns the premiums paid, plus interest. After that time, the full death benefit is paid. This is an important detail to be aware of when assessing policies while taking into account pre-existing diseases.

Key Factors to Consider When Buying Life Insurance for Parents

Deciding on a policy is a major decision. You have to take a few things into consideration carefully. It’s not only about being able to pick the cheapest plan. It’s a process of fitting the situation to the right needs of your unique family.

Taking the time to evaluate these things will result in a better outcome. You’ll be more confident in the decision you have made. That way you will know it’s the policy you want will do its job when the time comes. Let’s examine the most important things to consider.

Assessing Your Parents’ Health and Age

Age and health are the two largest factors that have an effect on life insurance. The younger and healthier the person is, the lower his or her premiums will be. This is why it’s always better to purchase insurance sooner than later.

Be honest about the health history of your parents. Do they smoke? Do they have long-term illnesses (diabetes, heart disease, etc.)? Insurance firms will ask the following questions. It’s better to be ahead of the curve to avoid being plagued down the road. This information will help find the companies and products that are the best fit.

Determining the Right Coverage Amount

How safe is the coverage that you need? It’s a common question. The answer is personal. It depends upon what you want the insurance to achieve. You do not necessarily need a million-dollar policy. A smaller policy that can still be very helpful.

This can be done using a very simple method to obtain a rough estimate. Think about Debts, Income, Mortgage, education/End-of-life costs (DIME). Add up what it would take to spend these expenses. This will provide a target amount of coverage. The goal is not to give so much that there are financial hardships, but just enough to not have financial hardships.

Coverage Calculation Checklist

-

Final Expenses

Estimate costs for funeral, burial, and any outstanding medical bills.

-

Outstanding Debts

List all debts like mortgages, car loans, and credit card balances.

-

Income Replacement

If a parent is working, how many years of income need to be replaced?

-

Legacy Gift

Consider any extra funds you’d like to leave for children or charity.

Understanding Policy Riders for Enhanced Protection

Riders are included as optional add-ins to a life insurance policy. They include extra benefits or coverage. While they can be a supplement to the price, there are riders out there who present incredible value. They will be able to tailor a policy to your own requirements.

One popular one is the Accelerated Death Benefit rider. It gives you access to a percentage of the death benefit while your parent is still alive, if he/she is diagnosed with a terminal illness. Exploring these add-ons is as important as knowing riders in life insurance themselves. This can bring much needed funds for care.

The Application Process: A Step-by-Step Guide

Applying for Life Insurance for Parents may seem intimidating. But it’s usually more simple than you think it is. Breaking it down and making it manageable by taking steps. The following is a basic guide to the process.

Step 1: Gathering Necessary Information

First, it will require that you collate some basic information. This includes your parent’s full name, date of birth, and social security information included. You will also need information about his or her medical history. Write down any doctors that they see, and any medications that they take.

Step 2: Getting Quotes and Comparing Companies

Hold off going with the first company you find. Shop around. Get quotes from a number of different insurers. Compare their Prices and policy features. Pay attention to the financial strength and reputation of the company. Choosing from the best life insurance companies can make a big difference in the run. An independent agent can help a great deal in this direction.

Step 3: The Medical Exam (If Required)

Many policies are demanding to provide you a medical exam. This is a common component of underwriting. A paramedic will arrive to your parent’s house. They will measure their height, weight and blood pressure. They also will take a blood and urine sample. It is an easy and fast procedure.

Step 4: Policy Approval and Review

After the exam, the application will reviewed by the insurance company underwriters. This can take several weeks. Providing they are approved, they will send you the final versions of the policy documents. Review them carefully.

The details of such a deal are crucial, so be sure all are right before you accept and make the first payment. Knowing how an insurance process works even for other forms such as learning how to file a car insurance claim, can make you comfortable with the system.

Addressing Common Concerns and Misconceptions

There are many who are hesitant to purchase Life Insurance for Parents. This is generally because of some common myths. Let’s go ahead and address these concerns. Understanding the truth can help you to make a sure decision.

“My Parents Are Too Old for Insurance”

This is a very common belief. But it’s often not true. Whereas choices can be more limited with age, they still exist. Senior insurance products, such as final expense insurance, are products that are written specifically for older adults. Even a small policy makes a huge difference. Some coverage is always better than none at all.

“It’s Too Expensive”

Another significant issue is cost. People assume that life insurance is out of reach in terms of cost. This is especially the case for the older applicant. While this does cost more for seniors, it may turn out to be less expensive than you think. There is no limit to having a final expense policy for such a cost, which is as small as a daily cup of coffee. Compare that to the thousands of dollars that a funeral may cost.

Peace of mind is not a luxury it’s a necessity. And sometimes, its price is much less expensive than the cost of worrying.

“We Have Savings, We Don’t Need It”

It is wonderful to have a healthy savings account. But, it shouldn’t be the main plan for final expenses. Such events as a major medical event or a long-term care stay can drain savings very quickly. Protection of those savings is provided by life insurance. It ensures that the money that your parents saved for their retirement is used for living not dying. It maintains intact their financial legacy.

The Ripple Effect of No Insurance

-

Sudden Loss

-

Immediate Funeral Costs

-

Savings Depleted

-

Debt & Stress for Family

Life Insurance as a Tool for Family Protection and Legacy

Let’s shift our perspective. Think of life insurance not as a morbid necessity, it is a powerful tool. It is a tool for love, family protection, and to leave something behind. It is one of the deepest gifts you can help your parents to give. This is a final act of care.

This is a way in which your parents can say, “I’ve got you covered.” It enables them to provide for their spouse’s protection. They are also allowed to have something to leave behind to their grandchildren.

It is a powerful statement. Broadening this concept of protection, it’s worth noting that there are many ways in which you can make your loved ones secure, and one of the ways to do this is to explore some of the top health insurance plans for families.

Creating a Financial Safety Net

Life is unpredictable. That is its only certainty. A life insurance policy serves as a buffer from this uncertainty. It’s a sure source of funds that is available almost immediately. This money is also free from taxation which is a big benefit provided by the financial experts on the site, Investopedia.

This is a safety net to keep your family afloat financially. They’ll not have to make rash decisions under pressure. They can pay the bills. They can stay in their home. It gives them the gift of time and stability to them most needed. Some policies are individual while others are group policies and understanding the difference between group vs individual policy can also help you make insurance decisions.

Leaving a Meaningful Legacy

A legacy is more than just a sum of money. It is about the values and love you give down. A life insurance policy can be an actual manifestation of that legacy. The death benefit can used for so many positive things. It can provide them a grandchild’s college education.

This could be a down payment on a first home. It may even be a donation to a favorite charity. As the National Council on Aging admits, planning your legacy is an important component of senior financial wellness. This way, the effects your parents have can felt for years to come. It leads to a financial product becoming a lifetime memory. Understanding your policy’s benefits such as no claim bonus in health insurance can further add to the value you receive.

“What you would eternalize, not that is engraved in stone monuments, but in the lives of others.

– Pericles

Taking the Next Step for Your Family’s Future

We’ve covered a lot of ground. You now have an idea of why having a Life Insurance for Parents is so important. You are aware of the various kinds of policies. The factors to take into consideration are known to you. The most important process is the next one – acting.

Don’t let this another article you read. Use this information to Strike Up a Conversation with Your Family. It may not be easy but it’s a conversation based in love and care. The peace of mind that it gives you is priceless. As a resource, the National Association of Insurance Commissioners (NAIC) is a source of unbiased information for consumers.

Start by getting some quotes. See what the options are. You may delighted by the low cost. Protecting your family’s future is a strong and responsible deed. It is a decision you won’t ever regret making (with your family).

Frequently Asked Questions

The best age is always young and healthy as possible to get the lowest rates. However, there are good senior insurance available even for those in their 60s, 70s, and 80s. The key is to act now.

No. The policy must not be forgotten-your parent must be aware of the policy and must sign off on the application. You can pay the premiums but they must agree to the cover. This is known as “insurable interest.”

In almost all cases the death benefit is paid to beneficiaries 100% income tax free. This makes it a very effective method of transferring wealth or paying snipes.

They can still get coverage. Options could be a “guaranteed issue” policy that doesn’t ask health questions or higher premiums but simplified issue policy. It’s best to work with an agent who can try to find insurers that will be more lenient with their condition.

The cost varies considerably depending on age, health, amount of coverage and type of policy. A healthy 65-year-old may manage to get a $25,000 final expense policy for $100-$150 per month. A term policy for a younger parent may well be much less.