Health Insurance Coverage for Mental Health Explained

Navigating the world of insurance can be really tough. However, we are here to help you understand your Health Insurance Coverage. Specifically, let’s talk about mental health. Your well-being is incredibly important. In fact it’s just as vital as your physical health. Therefore, knowing what benefits you have are the first step.

With this guide, I will tell everything to you. For example, we are going to explore what is covered. Furthermore, we will teach you how to use your plan. As a result, you can receive the support that you deserve. So I hope we will start this journey together.

The Growing Importance of Mental Health Insurance Coverage

Mental wellness is a huge part of your overall health. For a long time, it was sadly overlooked. However, times are changing for the better.

Why is Mental Health a Priority Now:

Awareness regarding mental health has increased tremendously. Consequently, people now know its effect on the day to day life. For example, it influences work, relationships and happiness. As a result, demand for care has exploded.

Insurance companies have definitely noticed this move. Therefore, they are now made to give better support. This is an enormous hope for all people. Your mind after all deserves the care you can possibly provide.

Understanding the Shift in Insurance Policies

Years ago, it used to be hard to get mental health insurance. Indeed, many plans provided very limited assistance. Some provided no coverage whatsoever. This in turn left a lot of people without options.

Thankfully, with new laws the landscape has changed. These laws make mental health something that must be taken seriously. For instance, they require fair coverage. We are going to get into these laws next.

Key Legislation Affecting Your Health Insurance Coverage

A major turning point was in the Mental Health Parity and Addiction Equity Act (MHPAEA). This law is a game-changer in the area of Health Insurance Coverage.

What is the MHPAEA:

The MHPAEA is a federal law that was passed in 2008. Its major objective, in short, is to assure fairness. It says that insurance plans cannot be more restrictive in nature for mental health compared to physical health.

This means that your copay should be similar. Also, visits to limits should not be stricter. In essence, it requires equal coverage from all insurance policy.

How MHPAEA Affects Your Health Insurance Plan

This legislation affects the majority of health insurance plans. This includes a lot of employer-sponsored plans. In addition, it also applies to plans purchased on the marketplace.

However, some plans could be exempt. For this reason, it is always wise to check your specific insurance policy. Understanding your rights that you possess is extremely important. Consequently, you are able to advocate for the care you need. Moreover, it is to help you in picking the right individual policy.

“There is no health without mental health.”

– David Satcher

Decoding Your Health Insurance Coverage for Mental Health

Your plan documents may appear confusing. Indeed, they are often full of technical terms. Let us now break down the process of how to find out what you need.

How to Find Your Mental Health Benefits

The first thing you should do is find your Summary of Benefits and Coverage (SBC). This document is your no. 1 best friend. Every insurance policy has to offer one.

Next go individual educational path, look for a section about “Mental/Behavioral Health.” This area will give you the information about the coverage details. For example, it includes the list of what services are included. It also demonstrates your possible costs. If you can’t find it just call your insurer.

Common Insurance Policy Terms Explained

Being able to speak insurance language is very important. Ultimately it helps you know your actual costs. Let’s look at a few key terms.

Deductible

A deductible is the amount of payment that you pay first. You have to pay this before your insurance starts paying. For instance, if you have a $1,000 co-pay, this means that from the services that are covered you will pay the first must of your insurance or out of pocket.

Copayment (Copay)

A copay is a set fee for a service. You normally pay this every time you visit a doctor. For example, you may have a $30 copay with each therapy session.

Coinsurance

Coinsurance – is a percentage of the cost. You are paying this after the amount of your deductible. For example, when your coinsurance is 20%, it means that you pay 20% for the bill. The other 80% is then paid on by your insurer.

Mental Health Insurance: At a Glance

What’s Usually Covered

- ✔️ Psychotherapy & Counseling

- ✔️ Inpatient Hospital Stays

- ✔️ Medically Necessary Screenings

- ✔️ Prescription Medications

- ✔️ Telehealth/Virtual Therapy

What Might Have Limits

- ❌ Experimental Treatments

- ❌ Out-of-Network Providers

- ❌ Services without a Diagnosis

- ❌ Marriage Counseling (often)

- ❌ Non-Essential Services

Types of Services Your Health Insurance Coverage Typically Includes

Your Health Insurance Coverage can open a lot of doors. In fact, it links you with a lot of helpful services. Let’s assume an exploration of the most common ones.

Therapy Insurance Coverage for Psychotherapy and Counseling

This is often referred to as “talk therapy.” It is without a doubt a cornerstone in mental health treatment. Therefore, most provisions of insurance plans cover it.

You can visit a psychiatrist, a psychologist or a therapist. These sessions help you deal with the way you feel. They also give you ways of coping. Your plan will cover your therapy insurance coverage.

Inpatient Services for Intensive Treatment

Of course, at times, more intensive care is required. Inpatient services refers to living at a hospital. This is if the issue is acute or severe.

This should be covered by your Health Insurance Coverage. Generally, it is treated like any other hospital stay. However, you may first require pre-authorization. This simply means that your insurer has to approve the stay prior to the stay.

Outpatient Services: Flexible and Accessible Care

Outpatient care is quite common. In particular, you go to a clinic or office for treatment. Then, you come home the same day.

This which includes therapy sessions and support groups. In addition, it also addresses intensive outpatient programs. These provide greater structure than do weekly therapy. It’s a flexible option for a large number of people. Plus, this is something you may want to explore if you are looking at health insurance plans for families.

Prescription Drugs Within Your Health Insurance Plan

Medication can be a important segment of the treatment. Indeed, in fact, it is used often with therapy. A list of covered medications along with the cost of a medicine is in your plan’s drug formulary.

A formulary is basically a list of approved drugs. You should refer to this list for your individual drugs. Costs may vary depending on drug tiers. For example, generic drugs are generally cheaper.

The Rise of Telehealth and Virtual Therapy Coverage

Telehealth has become immensely popular. It enables you to get care from meets. Specifically, however, you can speak to a therapist by video call.

Most insurance plans currently cover telehealth. It is convenient, private and effective. This is a great modern advantage of behavioral health coverage.

Insurance Policy Exclusions: What Your Plan Might Not Cover

While coverage is better, it’s not at all unlimited. For this reason, you need to take knowledge of the common exclusions. This helps to avoid the surprise bills.

Understanding Your Plan’s Insurance Policy Limitations

There are limits to each and every health insurance plan. For instance, there may be a limit on therapy sessions. You could have we’re only covered by insurance for 20 visits per year.

For this reason, be sure to read the details of your policy carefully. Knowing these limits is useful in helping you plan your care. You are also allowed to appeal for more sessions if necessary.

Experimental Treatments and Coverage

Insurance does tend to cover the proven treatments. On the other hand, it usually does not cover experimental ones. These are therapies that are still in the research stage.

If a provider recommends any sort of experimental treatment, try to find out ahead of time from your insurer first. Otherwise you will likely have to pay for it yourself. It may always be better to be sure, however.

The Importance of a Diagnosis for Coverage

The general requirement for insurance to pay is a diagnosis. This must be provided by a qualified professional. This is for conditions that have been included in the DSM-5.

Services such as general life coaching are not covered. This is because they are not medicinal treatments. This is an important distinction to keep in place.

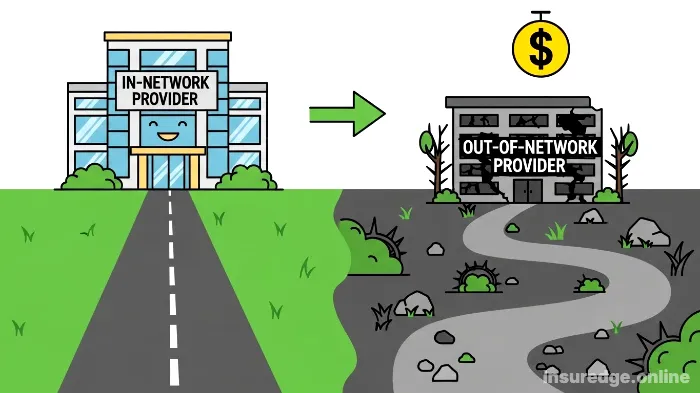

Out-of-Network Providers and Your Health Insurance Costs

Your plan has a network of providers. These people are known as in-network providers. Seeing them costs you less.

You can, of course, visit out-of-network care providers. However, its cost would be much higher. Your Health Insurance Coverage for them is less. In fact, sometimes, it is gets not covered at all. Whether to invest in term insurance vs whoelife policies can also affect your overall financial planning towards such a kind of expenses.

“The first step toward change is awareness. The second step is acceptance.”

– Nathaniel Branden

How to Maximize Your Mental Health Insurance Benefits

You pay for your insurance. Therefore, you should make the most out of it. Here are some tips to get the most for your money.

Finding In-Network Mental Health Providers

Always begin by locating an in-network provider. It is a good idea to use a search tool that is on your insurer’s website. Visit to locate therapists in your field.

Another great option is to call your insurance company. Specifically, they can provide you with a names list. This is the sure-fire way of keeping your costs down.

The Process of Getting Pre-authorization for Care

Some services require a pre-authorization. This is quite common regarding inpatient stays or some tests. It is usually the case with your provider’s office taking care of this.

Specifically, they take paperwork from your insurer. The insurer then considers the request. They endorse it if it is medically necessary. In short, it is an important step in the management of your care.

Navigating Claims and Denials with Your Insurance

After a service, a claim is lodged. Your provider sends a general bill for you. Your insurer then handles and dispels your claim.

Sometimes, however, a claim is not accepted. Do not panic if this happens. You have the right of appeal against the decision. In fact, many people succeed in their appeals. Knowing how to file a car insurance claim can give a broad idea about the claims process which is almost similar in health insurance.

How to Appeal a Denied Health Insurance Claim

First of all, determine why it was denied. The insurance company has to provide you with a reason by letter. Then, you should bring your medical records.

Next, write an appeal letter. Explain the service that was needed. Your provider can assist you in this regard. Following the process gives you the good chance. You should also check your company’s high claim settlement ratio as this is an indication of their reliability.

Finding Your Path to Coverage

Step 1: Review Your Plan Documents

Find your Summary of Benefits (SBC). This is your primary guide.

Step 2: Call Your Insurance Provider

Ask specific questions about therapists, copays, and session limits.

Step 3: Check the Provider Directory

Use your insurer’s website to find approved, in-network professionals.

Step 4: Confirm with the Therapist’s Office

Before your first appointment, call to confirm they accept your specific plan.

Choosing the Right Health Insurance Plan with Mental Health Benefits

If you are planning to switch to a new plan, however, mental health should be taken into consideration. A little research now after all saves a lot of stress then.

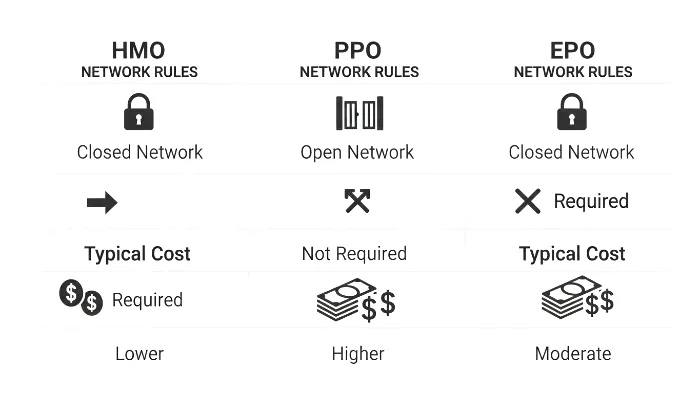

Comparing Different Health Insurance Plan Types (HMO, PPO, EPO)

Different Plans have Different Flexibility Levels. For this reason, it is important to know about the main types.

- HMO (Health Maintenance Organization): HMOs require you from using there network. In addition, you also need a referral to visit a specialist. Often, they can have lower premiums.

- PPO (Preferred Provider Organization): There is greater flexibility using PPOs. For example, you get to see out-of-network care providers. However you will pay a higher price for it. You do not need some referrals to specialists.

- EPO (Exclusive Provider Organization): EPOs are a mixed. You must stay in-network. But you do not require referrals for specialists.

Consider what you know to be important to you. Does it have a low premium or provider choice? Your answer will lead to your decision sooner or later. Many people think of life insurance early to get a better rate, a similar line of thought applies here as well.

What to Look for in a Family Health Insurance Plan

When profiling a whole family, needs are multiplied. You should therefore seek plans that have a strong provider network. Make sure there are children and adolescent specialists.

Also look in the family deductible. This is what you must pay in full before you can have everybody covered by the coverage. A good health insurance plan is essential to the peace of mind of your family.

How Pre-existing Conditions Affect Your Coverage

Thanks to the Affordable Care Act (ACA) insurers cannot deny you coverage for pre-existing diseases. This includes mental health problems such as depression or anxiety.

This is a crucial protection for all of them. As such, you can obtain the care you need without the fear. You can find out more about how do pre-existing diseases affect premiums. The ACA has more information on their official site at HealthCare.gov.

The Role of Riders in Your Insurance Policy

Sometimes, your master plan is not sufficient. Luckily, it is possible to enhance it with add-ons. You may be interested in understanding riders in an insurance plan to get extra protection.

A rider is an add on to your insurance policy. It provides extra benefits. A critical illness rider for example might provide a lump sum if you were diagnosed with a serious condition. While many think of life insurance, similar concepts can apply to health plans for instance.

Special Considerations for Your Health Insurance Coverage

Mental health is a varied discipline. Thereafter, your Health Insurance Coverage might have specific rules for different areas.

Behavioral Health Coverage for Substance Abuse Treatment

The MHPAEA law also includes addiction treatment. In fact, it requires such services of parity in substance abuse. This is an important aspect of behavioral health coverage.

Coverage is in detox, inpatient rehab, and counseling. These services save lives. For more support and information, you can visit Substance Abuse and Mental Health Services Administration (SAMHSA).

Health Insurance Coverage for Children and Adolescents

Children’s mental health needs are distinct from one another. Your plan should include things such as play therapy. In addition to this, it should also include family counseling.

Look for providers that are pediatrics specific. Early intervention to the well-being of the individual. A good family plan therefore makes this possible. You can calculate the right coverage to meet all the needs.

Mental Health Care in College

College can be a stressful period. For this reason, many students face mental health challenges. Most of the colleges require students to have Health Insurance Coverage.

Many university health centers have counselors. These are very often free or low-cost. You should check on what your student health plan is covered on. It is, after all, a valuable resource for youths of adulthood.

“Anything that’s human is mentionable, and anything that is mentionable can be more manageable.”

– Fred Rogers

Your Mental Health Matters, and So Does Your Coverage

Taking care of your mind is not a privilege. It is actually a basic requirement. Your Health Insurance Coverage is a tool for you to do that.

Therefore, don’t be afraid to ask for help. Don’t be embarrassed to take advantage of your benefits. You are making an investment into your long-term health and happiness. The National Alliance on Mental Illness (NAMI) is a great resource to use in terms of advocacy and support.

Do not forget to review your plan on a yearly basis. Your needs may change. In addition, the benefits offered under your plan may change, as well. Being informed is empowering the asset of knowledge and making correct decisions. For example, a good no-claim bonus may be a great incentive in some plans.

You should have the right to good mental health care. Then, consult this guide to get your way around insurance. Take that first step to a healthy happy you. You are absolutely worth it.

Frequently Asked Questions (FAQs)

Generally, yes. Most plans are mandated by law (MHPAEA and ACA) to have some mental health insurance coverage. However, the amount of coverage varies. For this reason, one should always check the details with your particular plan.

The best remedy is to use the provider directory on your insurance company’s website. Or you can give the member services number on your insurance card to obtain a list of in-network providers.

If you have been denied, you are entitled to an internal appeal with your insurance company. If that doesn’t work, then you may ask for an independent third party to review your evaluation.

Yes, because of the fact that the therapy insurance coverage for telehealth services has now been provided by most insurance plans for telehealth services, especially in the wake of the Covid-19 pandemic. However, you still need to confirm with your plan just in case.

Yes, absolutely. Thanks to the Affordable Care Act (ACA), it is illegal for an insurance policy to either deny you coverage or charge you more fees for your insurance on the basis of a pre-existing disease, including mental health conditions.