Tax Benefits of Health Insurance Under Section 80D

Are you paying hefty insurance each year for health insurance premiums? Do you know that you can save a lot of taxes? Section 80D in Income tax act provides significant benefits. Many taxpayers forgo these deductions. Today we have come to alter that in you.

Health insurance Isn’t All about Medical Coverage Anymore. It’s also a smart tax-saving tool as well. Knowing about Section 80D can help to have a huge charge credit saved in taxes. You deserve to have more money in your pocket. And, what does this provision do you?

Compare the Group Health Insurance vs Individual Policy — Key Differences to find what suits you best. Also, learn How Pre-Existing Diseases Affect Health Insurance Premiums and explore Understanding No-Claim Bonus in Health Insurance to maximize your savings.

Understanding Section 80D Tax Deduction

Section 80D gives deduction benefits on payment of health insurance premiums. This one can be claimed using the Income Tax Act, 1961. The provision covers the premiums paid for yourself, your spouse, children and parents. This tax deduction is available for individual and family floater policy premiums.

The government introduced this section to encourage health coverage. Medical inflation is increasing at alarming rate now a days. Healthcare costs can ruin your savings if you do not have proper insurance. Section 80D benefits helps to make health protection more affordable by saving through tax savings. You get double benefits – medical security and lower tax liability.

Tax Deduction Certificate

- Self & Family (Below 60 years) ₹25,000

- Self & Family (Senior Citizens) ₹50,000

- Parents (Below 60 years) ₹25,000

- Parents (Senior Citizens) ₹50,000

Who Can Claim Health Insurance Tax Benefits?

Any person paying for taxation in the form of income tax can claim for Section 80D deductions. You must be paying premiums for a medical insurance. It should be a policy that is in your name or in your family. The Hindu Undivided Families (HUFs) are also entitled to these benefits.

You can make a claim for you and your dependents. Your spouse and dependent children are under this provision. In addition, you can claim for your parents, as well. They do not have to be financially dependent on you. Senior citizens receive greater limits on deductions under this section.

Eligibility Criteria for Section 80D

The insured person has to be an Indian resident taxpayer. You can’t take deductions for siblings or in-laws. The health insurance premium should be paid via non-cash modes. Cheque, credit card, debit card or net banking are made acceptable. Cash payments do not qualify for tax deduction benefits.

The policy needs to be active and premium made. You need to maintain proper payment receipts all the time. Insurance companies issue tax statements with annual premiums. These are documents prepared when filing income tax returns. Your CA or your tax consultant will require them.

Maximum Deduction Limits Under Section 80D

The tax deduction limit depends on age groups. Individual taxpayers under the age of 60 years are eligible for a claim of ₹25,000 per year. This includes premiums for self, spouse and children. People belonging to senior citizens age group i.e. 60+ years get benefit of ₹50,000 deduction. This was the increased limit was given in recognition of higher medical needs in elderly individuals.

You can claim extra amounts for insurance for parents as well. If parents are below 60 then another deduction of ₹25,000. When the parents are senior citizens, this is increased to ₹50,000. The total amount for deduction reaches up to a value of ₹1,00,000 per annum. This occurs when you and the parents are both seniors.

As per Income Tax Department of India, these limits are excluding the expenses of preventive health checkup. You can use a combination of different eligible expenses to get the most from benefits. This is done with smart planning to get maximum deduction. We’ll talk about this strategy in detail later.

Deduction Breakdown for Different Scenarios

Let’s understand by examples for better understanding. For example, just this standard example, if you are 45 and parents are 65 then your combined deduction is at ₹75,000. This includes ₹25,000 for your family floater policy and ₹50,000 for parents. Where both you and parents are above 60, claim max of ₹1,00,000.

Young professionals with non senior parents get a total deduction of ₹50,000. Which gets split up as self and parents, i.e., ₹25,000 each. Some people have in-laws that come into Japan with the idea that that’s where they can cover in-laws; they’re not. The law lacks/knew clear definition of parents as biological or adoptive only.

What we have experienced and witnessed in all of this, I think everyone can agree on this, “Health insurance is not just about protecting your wealth; it’s about protecting your family’s future and peace of mind.”

– Financial Planning Expert

What Expenses Qualify for Tax Deduction?

Health insurance premium payments constitute the main qualifying expense. This includes individual policies or a family floater policy premiums. You can also claim for top-up and super top-up plans. Premium for critical illness insurance is also subject to this section.

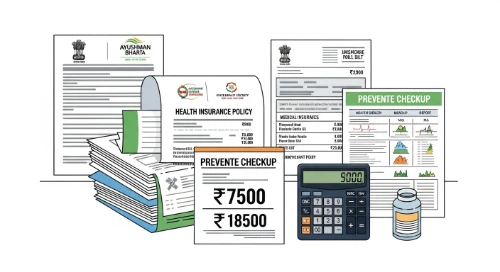

Preventive health checkup costs are separately deductible up to ₹5,000. This limit is inside the overall Section 80D ceiling as a whole. You do not have to have real medical bills about this part. Annual health checkups – diagnostic tests and screenings qualify here. Even cash payments are acceptable, for preventative checkups.

Medical expenditure relating to senior citizens who do not have insurance is also covered. If parents don’t have health coverage, real medical costs qualify. The same deduction limits are effective as with insurance premiums would. You must keep all bills and receipts of payments carefully. This provision ensures that elderly people don’t suffer without insurance.

Contributions to Government Health Schemes

The Central Government Health Scheme (CGHS) contributions are deductible as under Section 80D. Similar schemes for government employees are eligible for tax benefits. You can take these in addition to private insurance premiums. The amount added together shouldn’t exceed prescribed limits though.

Payments made to recognized health insurance funds also qualify. The insurance company must have regulatory approval. Insurance Regulatory and Development Authority of India (IRDAI) regulates these approvals. You should never buy policies without first checking the credentials of the insurers. Unauthorized schemes won’t provide you with any tax deduction benefits.

Eligible Expenses Checklist

-

Insurance Premiums

Individual, family floater, top-up plans

-

Preventive Checkups

Up to ₹5,000 within overall limit

-

Medical Expenses

For senior citizens without insurance

-

Critical Illness Plans

Standalone or rider premiums

How to Claim Section 80D Deduction

It is actually pretty easy to claim your tax benefits. These deductions will be declared in income tax returns. The process is somewhat different for salaried and self-employed people. Both categories are able to effectively maximize their tax savings though.

Know more about Understanding Riders in Life Insurance Plans and explore the Top 10 Health Insurance Plans for Families in 2025 for the best coverage. You can also read How to Calculate the Right Life Insurance Coverage for Your Family to make smart protection choices.

For Salaried Employees

Send your health insurance premium receipts to your employer. They will think of this when they are computing TDS (Tax Deducted at Source). These deductions would be reflected by your Form 16. This decreases tax deduction from your monthly salary itself.

While ITR filing on a yearly basis, mention premiums on the deductions section. You’ll find Section 80D appears in the deductions under the Gross Total Income category. Enter amounts paid for self, family and parents separately. Tax filing portal online calculates total deduction automatically.

For Self-Employed and Business Owners

You must keep detailed records of all payment of premiums. Turn in your returns with duly filed expenses. Choose ITR form correctly depending upon sources of income. ITR-1 or ITR-2 is an applicable general rule for most people.

Enter some accurate payment details in the Section 80D top column. Inclide documents (supporting) when done offline or as per required. The Income Tax Department can claim for verification at the time of assessment. Digital traces of payment enable verification is much easier and faster. Keep copies of all receipts in soft copy form for reference.

The Ministry of Finance periodically revises the guidelines that apply for claiming tax deduction. Keeping alive of policy changes would enable you plan better. Tax consultants can help you get through complex situations with great effect.

Preventive Health Checkup Benefits

Preventive health checkup deduction taxpayers are often unaware of. You can claim a maximum of up to ₹5,000 on your annual expenses. This is factored into total Section 80D of your combined further limit. Early detection of the disease can save a huge amount of medical costs later.

Annual health screenings, blood tests and diagnostic procedures fall into this category. Full body checkups provided by hospitals are eligible too. You do not have to issue receipts to each member of the family. Having a consolidated bill for the whole family works okay.

Why Preventive Checkups Matter

Regular health monitoring avoids the development of serious medical conditions. The earlier the intervention the less complex and most cost-effective the treatment, whether in terms of delivering and managing the treatment or in terms of costs. With policies, there is a tendency amongst insurance firms to offer free annual checkups. You can still claim the market value of these checkups.

Many corporate health insurance plans cover free screenings for preventative purposes. Checkups are even when your employer foots the bill. The tax deduction is used to offset other medical costs that are not covered by insurance. Smart taxpayers can effectively combine insurance benefits and tax planning strategies.

The saying goes, “An ounce of prevention is worth a pound of cure – and that goes for health management as well as wealth management.”

– Benjamin Franklin

Senior Citizen Special Benefits Under Section 80D

Senior citizens are given preferential treatment under the provisions of Section 80D. The deduction limit is doubled to ₹50,000 for people above 60. This recognises the increased healthcare needs of the elderly individuals. Medical inflation affects seniors with chronic health conditions especially.

If your parents are seniors then assert to claim ₹50,000 from their insurance. Even if they don’t have insurance, their actual medical costs qualify for deduction. Hospital bills, price of medicines, diagnostic charges are all included. Maintain appropriate receipts and prescriptions of all medical expenses.

Very Senior Citizens (80+ Years)

People 80 years and above are called very senior citizens. They receive the same limit of ₹50,000 in deduction currently. However their medical expenses tend to be much higher. The government periodically reviews these limits according to healthcare inflation.

Some elderly people are unable to afford health insurance because of their age. Pre-existing conditions render insurance prohibitively costly or unaffordable as well. The medical expenditure provision under Section 80D helps them to great extent. You can claim for legitimate medical bills in lieu of premiums.

Tax Planning Strategies to Maximize Deductions

The complete Section 80D benefits can be used well with the help of strategic planning. Many taxpayers fail to claim their entire amount of eligible deduction. Knowing different combinations helps to save a lot of tax savings. We are going to discuss some of the strategies that can be used by you now.

Family floater policy premiums are sometimes higher than the individual deduction limit. In such cases, it is worth considering separate policies for different members of the family. A mix of self and parent cover for maximum tax deduction benefits. This approach requires careful premium and coverage balancing though.

Combining Different Insurance Products

Get a basic health cover and add up plan. Both of these premiums qualify together for Section 80D deductions. Should add critical illness insurance riders to be fully covered, tax favorable. Medical insurance on certain diseases also counts against the limit.

Dental and vision insurance premiums are generally not subject to separate qualification. They must be included in comprehensive health insurance coverage. Accident insurance or personal accident covers do not come under Section 80D. Only health and medical insurance products are eligible for such deductions.

According to The World Health Organization good health coverage averts financial catastrophe. Coverage and tax benefits combined make insurance more affordable. This twin benefit creates incentive for more people to achieve health protection.

Common Mistakes to Avoid

Many taxpayers make avoidable mistakes when they exercise Section 80D deductions. Paying as premiums in cash are most common error. Cash payments automatically disqualify you from taking any tax benefits. Premiums should always be done through the digital or banking routes.

Claiming for ineligible relatives is another common mistake here. Brother, sister, in-laws and grandparents don’t qualify under current rules. Only your parents, spouse and dependent children are covered. The Income Tax Department will reject someone else’s claims.

- Missing documentation: Always keep top-notch receipts and policy documents in a secure manner throughout the year.

- Wrong amount claims: Not to take more than prescribed amount for your age category and family composition.

- Late premium payments: Make payments before the financial year end to get deduction in the current financial year of assessment.

- Ignoring preventive checkups: Make use of the utilization of the yearly health screenings and diagnostic tests through the healthcare allowance of ₹5,000 offered to them.

Documentation Requirements

Keep all the payment receipts for easy tax file. Insurance companies offer annual statements of premiums on request. Download these documents via the portals or mobile applications of insurers. Digital records are as valid as the physical copies today.

Medical bills for senior citizen expenses require detailed documentation. Hospital discharge summaries, pharmacy bills and test reports are a necessity. Prescription copies are a good way of helping with your medical expenditure claims. These may be verified by the tax department on assessment proceedings.

Critical Don’ts for Section 80D Claims

Never Pay in Cash

All premium payments must be through banking channels. Cash payments completely disqualify your deduction claims.

Don’t Claim for Ineligible Persons

Siblings, in-laws, and extended family don’t qualify. Only parents, spouse, and dependent children are covered.

Avoid Exceeding Prescribed Limits

Know your category’s maximum deduction. Claiming excess amounts raises red flags and invites scrutiny.

Impact on Your Overall Tax Liability

Section 80D deduction directly reduces the amount of your taxable income. This lowering of taxes can place you on a down tax bracket. The impacted saved tax will depend on what your tax rate will be. Taxpayers in the higher income bracket save higher absolute rupees.

To an individual with a 30 percentage tax rate, ₹50,000 write off would save ₹15,000. Multiply surcharge and cess and you save even more. Middle-class taxpayers (20% bracket) thus continue to save ₹10,000 in a year. Even 10% bracket taxpayers benefit through saving of ₹5,000rs.

Combining Section 80D with Other Deductions

Section 80D works further with other tax saving investment and expenses. PF, ELSS, and insurance are all eligible under deductions of 80C. The Section 80D benefits are in addition to the ₹1.5 lakh 80C limit. This deduction points down quite a lot of your taxable revenues.

Section 80D should not be mistaken with employer-provided medical reimbursements. Medical reimbursement is a whole other salary component as well. Both benefits may be claimed together for the maximum amount of tax savings. Strategic use of all of the deductions available to you optimizes your take home salary.

Recent Changes and Updates in Section 80D

Tax laws are adjusted periodically to keep up with economic reality. Section 80D limits have not changed significantly in the last few years. However, the eligible expenses and documentation requirements change constantly. To keep informed is to make sure not to miss out on new benefits.

The government has made it easy to digitally submit claims of tax deduction of taxes. Pre-filled ITR forms now contain insurance premiums data automatically. This information goes directly from insurance companies to tax portals. Check these auto-populated details before putting your return through though.

Digital Health Records Integration

India is progressing towards connected digital health data records. These will tie health expenditure to tax filing automatically. Claim processing will also become faster and more transparent in the near future. You’ll spend less time collecting documents by hand any more – each year.

E-insurance policies have become a standard throughout the industry. Digital premium receipts are just as valid as the physical ones. Download and store these receipts to the cloud for safety. Always password protect folders that have sensitive information, such as financial information and health information.

Health Insurance Beyond Tax Benefits

While tax savings are appealing, health coverage is the major objective. Don’t get insurance to claim Section 80D deductions. Positive medical insurance cushions your family against an economic crisis. Rising health care costs can drain lifetime savings with no insurance.

Select the policies depending on the areas of coverage rather than the premium, amount. Higher sum insured helps in giving better protection against medical inflation. Test insurance companies in terms of ratio of claims settlement and customer service. The lowest-cost premium is not necessarily the best insurance deal.

Choosing the Right Health Insurance

Assess your family history and the needs of your family members carefully regarding medical concerns and needs. Consider immediate needs as well as possible future medical needs. Senior citizens require higher coverage because they have age-related health issues. Young families are supposed to plan for maternity and children healthcare coverage.

Network Hospitals, cashless facilities, and Claims process matters very much. Consumer policy documents carefully before buying any insurance product. Know about exclusions, waiting periods and sub-limits on different treatments. An informed decision does not only keep you better protected than tax-motivated purchases.

“The best time to purchase health insurance is when you don’t need it yet — because by the time you need it, it may be too late.”

– Insurance Industry Wisdom

How Section 80D Promotes National Health Goals

Government policies to promote health insurance tend to have larger social goals. Universal health coverage helps in reducing the burden on the public healthcare infrastructure. Section 80D benefits make it more affordable for middle-class families to have private insurance. More Insured Citizens, Better Health Nationally.

Tax deduction incentives have increased the insurance penetration significantly over years. More Indians are now covered by some form of health coverage. This shift lowers out-of-pocket medical spending for common people. Financial protection against health emergencies leads to a better quality of life in general.

Insurance Awareness and Financial Literacy

To understand Section 80D, basic financial literacy of taxation is needed. When the population is constantly informed, it gives them the skills to make wise money choices. Tax planning becomes an essential life skill and not expert territory. Educated taxpayers can make optimal financial decisions without paying high consultant fees.

Due to digital India projects, tax filing became available to all users. Taxpayers are assisted by online resources, tutorials, and helpline. You can do returns on your own with very little technical knowledge. This democratization of financial services serves the whole nation well.

Find out Term Insurance vs Whole Life Insurance — Which One Suits You Best? and Why Millennials Should Consider Life Insurance Early. Don’t miss the Best Life Insurance Companies with High Claim Settlement Ratio 2025 and learn How to File a Car Insurance Claim Step-by-Step for smooth claim handling.

Frequently Asked Questions

No, you can’t make tax deduction on your brother’s insurance premium. Section 80D only covers premiums made for self, spouse, dependent children and parents. Siblings don’t meet the definition of eligible family members on this provision.

No, it’s not necessary for claiming the expenses for preventive health checkup with the help of health insurance. You can individually claim not less than ₹5,000 for health checkups. This deduction is available as part of the overall Section 80D limit even if one does not have insurance.

There are no premiums for which you can say that you’ve paid because they were paid by your employer. But only premiums you pay with your own pocket have the Section 80D benefits. However, employer-provided group insurance doesn’t prohibit you from purchasing extra personal insurance and deductible those premiums.

No, life insurance premiums don’t qualify under Section 80D at all. Life insurance is under section 80C deductions instead. Only health insurance, medical insurance premiums are eligible for Section 80D tax benefits.

Yes, you can claim deduction for premiums paid in instalments. Make sure all payments are made using non-cash modes only. The sum total paid during the financial year is eligible for deduction. When filing for installment payment documentation, keep all receipts for these loans.

Section 80D has immense tax benefits when it comes to tax and you should not pass up on it. Understanding these provisions is an important assistance to save thousands in taxes every year. Combine smart insurance planning with optimization against the taxman.

Protect your family’s health and create your financial security at the same time. Begin investigation into existing health insurance plan coverage. Perform potential tax savings and make necessary policy adjustments prior to end of year 2. Memory and posterity will say you have made a good choice.

It is important to keep in mind that proper money management and good health are one and the same thing. Health insurance covers medical emergencies and alleviate tax burden. Take advantage of every rupee of deduction that you have available to you. Complex situations involve consulting a qualified tax advisor to give specific advice. It is now time to begin your health coverage and tax savings.