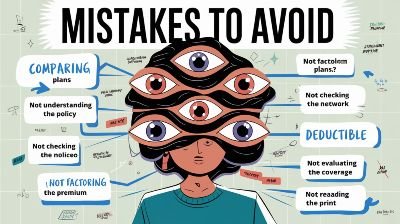

Top Mistakes to Avoid While Buying Health Insurance Online

Welcome! We are so glad you are here. In the today’s digital world everything is a click away. You can order food, purchase clothes, and even your finances. This easiness has now spilled over to securing our health. The process of buying health insurance online has become very popular. It seems easy and quick. But this ease can cause major mistakes at times.

These mistakes could cost you dearly. They can leave you without the cover you know you need most when you need it most. You don’t want to fall into any of these crosshairs, however. This will be a guide that will walk you through the biggest mistakes. You will learn how to make a well-thought-out and well-informed choice. Your health and your financial stability are just too important to gambling. Make we can make sure your digital policy is a lifeline – not a pain in the head.

Compare the Group Health Insurance vs Individual Policy — Key Differences to find what suits you best. Also, learn How Pre-Existing Diseases Affect Health Insurance Premiums and explore Understanding No-Claim Bonus in Health Insurance to maximize your savings.

Mistake 1: Not Reading the Policy’s Fine Print

This is the most popular error that people make. We are so often presented with a long document and we just click “I Agree.” This is a mammoth risk where insurance is concerned. The soul of a policy is in the fine print. It outlines what it covers and more importantly, what it does not cover.

Why the “Terms and Conditions” Matter

Each of the digital policy has a detailed document. It lists all the rules. It speaks of exclusions, waiting periods and sub-limits. When you skip on this you are buying a product blindly. And you may think one particular illness is covered. The fine print may say otherwise, however.

What to Look for Specifically

When reviewing the policy wording look for these key sections of the policy.

- Exclusions: This is a list of the treatments and conditions that the policy will not pay for.

- Waiting Periods: We will get into more of this later. It is that time you have to wait before you claim certain things.

- Definitions: Know how the insurer is defining such terms as “hospitalization” or “pre-existing disease.”

The legal jargon has no fear in you. Take your time. Use dictionaries on the Internet or call the insurer to clarify. A prudent manager will be grateful your future self,a diligent manager today will be grateful you.

“The time to repair the roof is when the sun is shining. The time to understand your health policy is before you get sick.”

Mistake 2: Focusing Only on the Lowest Premium

Everyone loves a good deal. It is tempting to organize plans by availability on the basis of “Price: Low to High.” However, buying the cheapest is a classic insurance shopping error. At times low premium is concealing substantial compromises in your coverage.

The Hidden Costs of a “Cheap” Plan

A policy with low premium could appear good. But it could have:

- A very high deductible. This is the amount which you pay before payment by the insurer is paid.

- Strict co-payment clauses. You are required to pay a percentage of each claim.

- A lower sum insured. This may not be sufficient for large-treatments.

- Fewer network hospitals.

So imagine being thousands of dollars off just a year on a premium. Then you have a bill in which you must pay 20% of a huge hospital bill. The cheap plan suddenly becomes very costly.

Balancing Cost with Comprehensive Coverage

The focus is on value, not a cheap price. Do not take advantage of online comparison services. Don’t just look at the premium. Comparing the characteristics with each other. A slightly more costly plan may have much better protection. It could save you your financial ass in the event of a medical crisis.

Here’s a simple comparison to illustrate the point:

| Feature | Plan A (Low Premium) | Plan B (Moderate Premium) |

|---|---|---|

| Annual Premium | ₹10,000 | ₹15,000 |

| Sum Insured | ₹3 Lakh | ₹10 Lakh |

| Co-payment | 20% on all claims | None |

| Room Rent Limit | Capped at ₹3,000/day | No Cap (Single Private Room) |

| Network Hospitals | 2,500+ | 8,000+ |

As you can see there is much more value and security offered in Plan B for a small increase in premium. This is a very important component of smart insurance shopping.

Mistake 3: Ignoring the Network Hospital List

An important advantage of the health insurance is the cashless facility. This means that the hospital charges the insurer directly. You do not need to fork out heavy sums out of your pocket. This facility is limited to network hospitals.

The Importance of a Good Hospital Network

While buying health insurance online, you need to check the list of network hospitals. What good is a policy if the best hospitals near your home are not in the list? You would be required to pay the entire bill first. Then you would file for reimbursement at a later date.

How to Check the Network

Every insurer’s web site contains a “Network Hospital Locator” tool. Use it.

- Enter your city and pin code.

- Check to see if there is a major, reputable hospitals in your area.

- Make sure that your favorite doctors or specialists consult at these hospitals.

A good insurer is one who has a good network. It demonstrates that they have established great partnerships. This way you have a better claim experience.

Mistake 4: Not Disclosing Your Full Medical History

This is an error caused out of fear. Some people are concerned that disclosing a pre-existing condition will make their premium higher. Or they are afraid that their application will be rejected. So, they hide information. This is a critical error.

The Principle of Utmost Good Faith

Insurance contracts are founded on a principle referred to as “utmost good faith.” It means you, as well as the insurer, must be totally honest. Hiding a medical condition could mean that your insurer will then refuse to cover you by rejecting your claim. They can even cancel your policy for being non-disclosure.

Know more about Understanding Riders in Life Insurance Plans and explore the Top 10 Health Insurance Plans for Families in 2025 for the best coverage. You can also read How to Calculate the Right Life Insurance Coverage for Your Family to make smart protection choices.

What Counts as a Pre-existing Disease (PED)?

A PED is any health condition you had before you purchased the policy. This includes things like:

- Diabetes

- High blood pressure

- Asthma

- Thyroid disorders

- Any past surgeries

You should be honest about yourself and your lifestyle as well. If you smoke or drink, tell him or her. It has an impact on your risk profile and your premium. An honest disclosure action is certain that your digital policy is sound and trustworthy.

Mistake 5: Overlooking the Waiting Periods

A health insurance policy does not take care of everything on the first day. There are waiting periods. This is a matter that often causes confusion. Failure to understand them may result in claim rejections and frustration.

Different Types of Waiting Periods

Your policy will contain a number of waiting periods. A claim for certain conditions may not be made during this time.

| Waiting Period Type | Typical Duration | Description |

|---|---|---|

| Initial Waiting Period | 30 Days | No claims are accepted except for accidents. |

| Pre-existing Diseases (PED) | 2 to 4 Years | Coverage for diseases you already have begins after this period. |

| Specific Diseases | 1 to 2 Years | Coverage for specific listed ailments like cataracts or hernias starts after this period. |

| Maternity Benefit | 9 Months to 4 Years | Coverage for childbirth and related expenses has a long waiting period. |

When you are buying health insurance online, look for policies with shorter waiting periods, particularly for pre-existing diseases. Some current policies are rolling back these to attract customers.

Mistake 6: Not Understanding Sub-limits and Co-payments

Sum Insured is the maximum payable amount by the insurance company in case of loss in a year. But within that limit there can be another limit. These are called sub-limits. They can have a huge impact on the amount the insurer will pay for a claim.

The Trap of Sub-Limits

A sub-limit is a limit that some particular expense can’t exceed. For instance, a policy with a sum insured value of Rs. 5 lakh may have a sub-limit on room rent. The uppermost limit of payment by him may be only up to Rs. 5,000 per diem for the room. If you decide on a room which is.conf Thomson’s simple checking Wen Raising what cost for Indians is 8000Destiny That you’re Decision the purchase of you to pay the Difference

Common sub-limits include:

- Room Rent

- ICU Charges

- costs of specific surgery (e.g. cataract surgery)

- Ambulance charges

The Role of Co-payment

Co-payment is a cost sharing provision. It involves committing to a payment of a certain percentage of the claim amount. For instance, if you pay 10% co-payment on a bill of Rs 2 Lacrupers are made to pay Rs 20000. The insurer pays ₹1,80,000. While plans with co-payments cost less per month, this does put more money out of your pocket. It’s wiser to go for a plan with zero co-payment.

Mistake 7: Failing to Compare Plans Thoroughly

Online comparison has become very easy with the advent of the internet. However, many people look at only one or two plans. They may choose a brand that they have heard of before. Or they simply pick the one recommended by their friend and do not do their own research.

How to Do an Effective Online Comparison

Yourreetletter campaign represents the thorough process of insurance shopping. Use a proper insurance aggregator website. These platforms allow rapid comparisons of dozens of plans at the same time.

Here is a simple process for effective comparison:

Ideal Insurance Shopping Process

Step 1: Assess Your Needs

- Take into account your age, family size and location.

- Consider your way of life, medical history.

- Determine a sufficient Sum Insured

Step 2: Shortlist 3-4 Plans

- Use an aggregator to filter in the plans based on your needs.

- Don’t just look at the price. Look at features.

Step 3: Dive Deep into Details

- Review the policy wordings and the brochures of the selected plans.

- Compare waiting times, sub-limits and hospital networks

Step 4: Check Insurer’s Reputation

- Claim Settlement Ratio (- look at this below)

- Read reviews and feedback from the customers.

Step 5: Make Your Choice

- Choose the most suitable package of features, service, and cost.

This guarantees that you are not simply purchasing a policy. This will give the appropriate protection to your family. A great resource for understanding global health financing systems is the World Health Organization’s page on Health Financing . It explains why a sound personal insurance coverage is so crucial.

Mistake 8: Neglecting Riders or Add-ons

Basic health insurance policy offers good coverage. However, your needs may be different. Riders, or add-ons, are optional benefits that you can purchase to add to your policy for a few dollars more. They make it possible to design your coverage the way you want.

Popular and Useful Riders

Many people neglect riders when shopping for insurance shopping. This is a wasted opportunity to create a really complete plan.

Some valuable riders include:

- Critical Illness Cover: Ensures a lump sum pay-out if diagnosed with critical illness such as cancer or heart attack. This money can be used to pay for expenses outside of hospitalization.

- Hospital Cash Benefit: Provides you with a fixed amount of money to you, based on the number of days you are hospitalized. It can also apply to incidental expenses.

- Maternity and Newborn Cover: A must if you are planning to start a family.

- Personal Accident Cover: Offers coverage in case of disability or death arising from an accident.

In many cases it is more cost effective to add the rider to a corresponding existing policy rather than taking out a separate policy for that particular requirement.

Mistake 9: Not Checking the Claim Settlement Ratio (CSR)

What is your greatest expectation of the insurance company? You want to get them to pay your claims. The Claim Settlement Ratio (CSR) is one of the important indicators of an insurer’s reliability. This is expressed as a percentage of the claims that the company has paid out.

Understanding CSR

The CSR is calculated as:

(Total claims payable / Total claim filed) 100

The higher the CSR is, the better. This implies that the insurer has a good history of fulfilling its promises. This information can be obtained from the annual report of the insurance regulator.

“Trust is built with consistency. In insurance, consistency is a high and stable Claim Settlement Ratio.”

Beyond the Numbers

Although a high CSR (preferably greater than 90%) is good, it’s not the only criteria. Also look at:

- Claim Rejection Ratio: The lower the rejection ratio is, the better.

- Average Turnaround Time: How long does it take the insurer to process the claims?

- Customer Reviews: What are Real Customers Saying About Their Claim Experience?

Image of service of the insurer – When combining these factors, you’ll have a holistic understanding of the quality of insurer services. A hassle-free claim handling is invaluable in a stressful medical emergency. For more insights on financial regulations, you could explore resources from financial watchdogs like the U.S. Securities and Exchange Commission (SEC) to understand the importance of regulated industries.

Mistake 10: Forgetting About Portability and Renewability

Your relationship with your health policy is for the long haul. Two key factors that should be considered are portability and lifetime renewability.

The Power of Portability

What if you are not happy with the service of your existing insurer? Health insurance portability is the ability to change insurers. You can do this without suffering the loss of benefits you accrued. This includes the prepayment of credit for waiting period for pre-existing diseases. Portability provides you with the bargaining leverage to get better service.

The Assurance of Lifetime Renewability

This is a crucial feature. A preferred shareholder meaning that the company insurer will promise to reauthorize your insurance every year despite your age or health. As you age, you will require more health insurance. Lifetime-guaranteed – a policy that fulfills its name and will continue to offer cover well into old age. Always choose a digital policy that offers this guarantee. For detailed consumer advice on insurance products, visiting a consumer protection agency site, like the Consumer Financial Protection Bureau (CFPB) , can offer additional guidance.

Buying Online vs. Offline: A Quick Grid

| Aspect | Buying Online | Buying Via an Agent |

|---|---|---|

| Convenience | High (24/7 access) | Moderate (Requires meetings) |

| Comparison | Easy (Multiple plans at once) | Limited (Biased towards certain plans) |

| Cost | Often cheaper (No agent commission) | Can be more expensive |

| Information | Full access to all documents | Information can be filtered by the agent |

| Guidance | Requires self-research | Personalized guidance available |

Conclusion: Your Path to Smart Health Insurance

The online purchase of health insurance is empowering. It places control directly in the hands of a person. But great power has to be meet with great responsibility. Avoiding these 10 common mistakes is all it takes to making a truly smart choice.

Therefore remember to look beyond the premium. Go into detail on your digital policy. Use online comparison tools wisely, and never fall back in asking questions. Certainly when you are looking to purchase insurance from any agency your aim is not merely to purchase a policy but to invest in peace of mind. By doing your due diligence and being a cautious consumer, you can find a health insurance plan that will be there with you through thick and thin. Take your time to research and get a policy which actually protects you and your family.

Find out Term Insurance vs Whole Life Insurance — Which One Suits You Best? and Why Millennials Should Consider Life Insurance Early. Don’t miss the Best Life Insurance Companies with High Claim Settlement Ratio 2025 and learn How to File a Car Insurance Claim Step-by-Step for smooth claim handling.

FAQs (Frequently Asked Questions)

Yes, it is completely safe. But make sure that you are purchasing from the official website of the insurer and from a reputed and certified insurance aggregator.

This will vary depending on your age, city of residence (healthcare is more expensive in large cities), number of family members and medical history. The ideal amount for a family in a metro city is a sum assured of at least Rs 10-15 lakh.

In general, the amendments can be made such as the inclusion of a new family member or sum insured addition at the time of renewal (splices addition cannot be made during the contract year).

Insurance companies offer a grace period (typically 15-30 days) for payments of the premium. If you do not pay within this time, your policy will end and all accumulated benefits will be forfeited.

At a network hospital, you should present your health insurance card at the front desk of the TPA (Third Party Administrator). They can deal with the pre-authorization and billing directly with the insurer.